The payment service provider Klarna recently launched a price comparison service for online shopping in Germany. Klarna is one of the big payment companies, but the current account has so far had few users.

(Photo: obs)

Frankfurt Fintech Klarna has established itself in the German financial system. But when it comes to current accounts, the Swedish company’s offer is still struggling: two years after it was launched, 215,000 current accounts were opened in Germany. Klarna gave this number when asked by the Handelsblatt.

This puts Klarna well behind other institutes. For comparison: the German savings banks, which belong to the traditional branch banks, recorded 650,000 new account openings last year alone. At the DKB, the number of private current accounts rose by almost 250,000 to 4.2 million in 2022.

ING managed around 3.1 million current accounts, around 150,000 more than a year earlier. The bank of the comparison portal Check24, C24, recently told the Handelsblatt that three years after it started, it only had around 100,000 customers.

The example underlines that current accounts from financial start-ups (fintechs) are not a sure-fire success – even when it comes to free offers and even when a large company is behind them. In this country, the competition among online and fintech banks is very fierce. In addition to providers such as N26, Vivid and Bunq, the large direct banks ING Germany, Comdirect and DKB also target online-savvy customers.

The institutes offer free checking accounts generally or under certain circumstances, usually with a minimum monthly payment. At Klarna, the use of the Klarna app is a prerequisite for a current account. The company only understands this to mean that you log into the app at least once a month. At the same time, you can also access Klarna payment methods without an app.

Klarna is struggling with the slump in the rating

Klarna is one of the leading international payment providers. The fintech is best known for its payment method – including invoice and installment purchase, in technical jargon “buy now, pay later” (BNPL). You can pay with Klarna at more than 500,000 retailers worldwide.

>> Read more here: Apple attacks banks and fintechs

The company has been trying to position itself as a shopping app for some time. Like many other young companies, what was once the most valuable listed start-up in Europe is struggling with the fact that the valuation has recently plummeted.

For the current account in Germany, Klarna uses its Swedish banking license, with which the fintech can offer banking services across the EU. So far, the giro account has only been available in Germany. In addition, Klarna has been attracting savers in Germany since the beginning of last year with high interest rates on fixed deposits.

Germany boss Nicole Defren emphasized that Germany is an important core market and still has “top priority”, “which is why we will continue to invest heavily here”. Sales in the Federal Republic, where Klarna has been represented for almost 13 years, rose by ten percent in 2022, while the e-commerce market as a whole shrank. However, the company does not give specific figures.

USA overtakes Germany as Klarna’s top-selling market

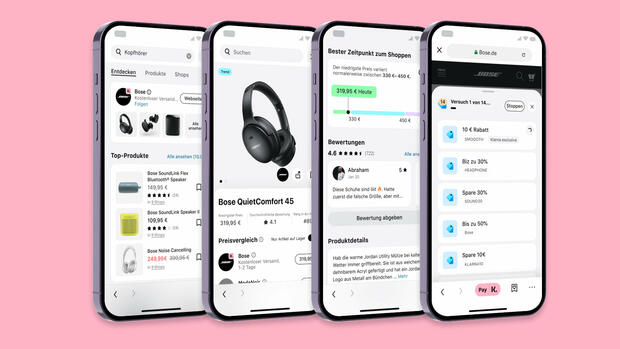

Last week, Klarna also launched a price comparison for online shops in Germany. Consumers can search for products from 3,800 retailers there, filtering by criteria such as colour, size, features and customer ratings. The price comparison is based on Pricerunner technology. Klarna took over the Swedish company in 2021.

From the point of view of Christiane Neumüller, payment expert at the consulting firm Capco, the price comparison fits in with the overall strategy because Klarna does not see itself primarily as a payment solution, but as an ecosystem around online shopping. It could also help to improve Klarna’s reputation again.

Germany has long been the most important market for the company, which was founded in 2005. At the end of 2022, however, the USA overtook Germany as the market with the highest turnover.

In the USA, where Klarna started in 2015, the company has eight million app users and a total of 34 million customers. There are six million active app users in Germany.

More: Allianz wants to sell shares in smartphone bank N26